Healthcare M&A Synergy Capture: The Procurement Blind Spot

Insights Article

A guide for CFOs, PE operating partners, and integration leads at mid-market healthcare companies

Mac Hodell Partner, Inside Consulting

Published June 5, 2026

Healthcare organizations executing mergers and acquisitions are leaving meaningful EBITDA on the table. The reason is not organizational chaos or cultural misfires. It is a systematic underestimation of procurement as a synergy lever. Understanding why that happens, and what to do instead, is the difference between a deal that merely closes and one that actually creates value.

The value creation problem in healthcare M&A

Healthcare consolidation continues at pace. Health systems, physician groups, outpatient platforms, and PE-backed services businesses are all active acquirers. Yet the financial returns are sobering. Disciplined health systems that apply systematic attention to synergy capture can achieve cost savings of 9 to 23 percent of the acquisition target’s cost base, but most fall well short of that range.

The challenge is not unique to healthcare. Harvard Business Review has documented M&A failure rates in the range of 70 to 90 percent across industries, and McKinsey research consistently identifies more than 60 percent of acquisitions as value-destructive for the acquirer. In healthcare specifically, failure rates run 75 to 80 percent by most analyses, higher than manufacturing and consumer goods, reflecting the sector’s operational complexity.

— McKinsey & Company, Capturing M&A Value: Cost, Capital, and Revenue Synergies

Bain & Company’s research reinforces this: only about 30 percent of acquirers report achieving their synergy targets, and overestimating synergies is the most frequently cited reason for deal failure among the executives Bain surveyed. The pattern is consistent: deals look promising at announcement, and value erodes after close.

SaaS now commands a material and growing share of enterprise IT budgets. In 2019, SaaS represented roughly 13 percent of total IT spend, a predictable line item dominated by per-seat licensing with stable renewal cycles. By 2024, that share had grown to 21 percent, driven by the proliferation of consumption and usage-based pricing models that introduce variability most finance teams were not built to manage.

Figure 1: SaaS as a share of total IT budget — 2019 vs. 2024

Denominator is total IT budget inclusive of hardware, labor, infrastructure, and services.

Source: BCG analysis of Gartner IT spend forecast data, as reported in BCG research on enterprise software procurement complexity, October 2025.

That shift in budget composition is not inherently a problem. The problem is that most organizations’ vendor management practices have not kept pace with it.

The predictable hierarchy of attention

Post-merger integration teams in healthcare follow a predictable priority stack. Organizational integration (reporting structures, leadership decisions, workforce alignment) consumes the most attention, and rightly so. McKinsey’s analysis of culture in integration planning found that roughly 75 percent of organizations that managed culture effectively reported meeting or exceeding their synergy targets, compared to around 45 percent of those that did not. Get the people side wrong and nothing else matters.

Below organizational integration, the next focus is almost always labor cost savings: headcount rationalization, benefit harmonization, and elimination of redundant management layers. These gains are visible, tangible, and often already anticipated in deal modeling.

Procurement synergies sit third on the priority list, and in practice they are frequently treated as an afterthought. The underlying logic is intuitive: combining two organizations creates greater purchasing scale, which yields better pricing. That logic is not wrong. It is simply incomplete, and the gap between “scale leverage” and genuine procurement value is where most organizations leave money behind.

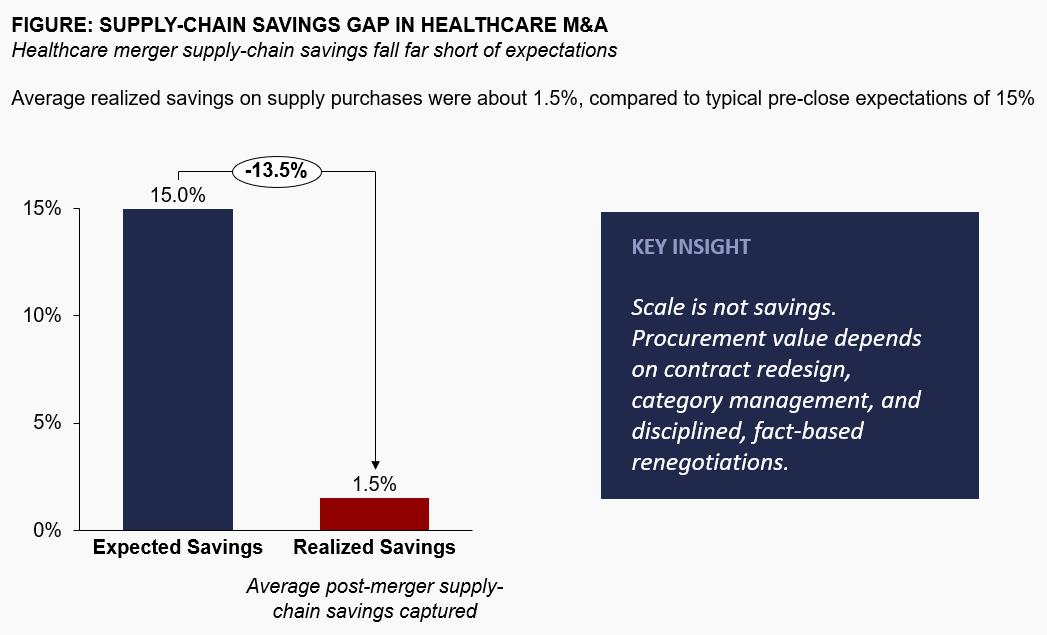

Hospital mergers often promise 15% supply-chain savings, but research shows actual realized savings average just 1.5%.

Source: NBER, “Mergers and Marginal Costs: New Evidence on Hospital Buyer Power”; Healthcare Finance News, summary of merger savings research.

Why procurement synergies underdeliver in healthcare

There are two structural reasons procurement synergies in healthcare M&A are systematically underestimated and underdelivered. Understanding both is essential to capturing more.

The scale leverage trap

The dominant logic in deal modeling is this: the combined entity has more purchasing power, therefore suppliers will offer better pricing. This is true as far as it goes. The problem is that this logic is also visible to every other bidder in the room. When increased purchasing scale is the primary procurement savings thesis, that value is typically priced into the acquisition bid before close. You are paying for the synergy without necessarily capturing incremental value beyond what was assumed.

McKinsey makes this point explicitly in its synergy capture work: rather than applying generic savings percentages to SG&A or procurement spend, credible synergy cases are built on functional deep dives and bottom-up planning, specifically in areas with the greatest value creation potential. The rigor required is higher than most integration teams invest.

The specificity problem in healthcare spend

Healthcare outside spend has characteristics that make generic procurement synergy approaches particularly unreliable. Clinical services, revenue cycle vendors, managed care contract administration, GPO arrangements, and specialty IT systems all have category dynamics that differ materially from one another. A savings lever that works for facilities management may be irrelevant for a tightly contracted clinical information system with prohibitive switching cost. Lumping these categories together under a single savings assumption, however logically derived, guarantees underperformance.

The solution is category-level analysis: understanding, for each significant spend category, which savings lever is actually operative. Not all spend responds to the same lever, and the mix matters enormously for what is actually achievable.

The three levers: which one is most underused

Across healthcare M&A engagements, outside spend responds to three primary levers. The strategic challenge is understanding which lever applies to which spend, and allocating integration effort accordingly.

1. Volume consolidation

This is the lever that deal models default to. When two organizations consolidate purchasing volume with a common supplier, they achieve better unit economics. It is real, measurable, and achievable within 12 to 18 months of close. The limitation is savings magnitude: for most healthcare spend categories, volume consolidation alone yields 3 to 8 percent compression, valuable but not transformational.

2. Demand management

This lever questions not what you pay per unit, but how many units the combined organization actually needs. In healthcare, demand management opportunities cluster around three areas: utilization of contracted services that were individually under-monitored, specification rationalization (are both organizations buying the equivalent product at different spec levels?), and service model efficiency (are you paying for managed services you could partially self-perform at scale?). Well-executed demand management can yield 10 to 20 percent savings on addressable spend, but it requires cross-functional engagement with clinical and operational leadership that most procurement-led integration teams do not secure.

3. Competitive displacement

This is the highest-value lever and the one most consistently underexplored. Competitive displacement means credibly threatening, and where warranted executing, a supplier transition. For spend categories where incumbent vendors carry embedded margin and where switching cost is manageable, the threat of a competitive evaluation produces results that volume renegotiation cannot. Savings rates of 15 to 25 percent are achievable in categories where displacement is credible. The prerequisite is category-specific intelligence: understanding vendor margin structures, competitive alternatives, and the specific aspects of the current specification that can be challenged or rationalized.

— McKinsey & Company, cited in Procurement Magazine

The practical implication is this: organizations that default to volume consolidation as the primary savings thesis capture a fraction of what is available. Firms that invest the additional analytical work to map spend against levers, and to build a credible competitive displacement capability, consistently outperform their own synergy targets.

A healthcare rollup case: US Eye

US Eye is a useful illustration. A PE-backed ophthalmology platform, US Eye added dozens of practices within an 18-month period. Vendor consolidation across core medical items, technology, and SG&A had not kept pace with the pace of acquisitions. The retail optical arm was one of several underconsolidated areas: it had no centralized purchasing strategy, sourcing product from more than 60 vendors with no coordinated portfolio logic.

Inside Consulting applied a mix of sourcing approaches calibrated to each category across the full outside spend base: direct negotiations in some areas, multi-round competitive tenders in others, live-bidding events where market dynamics supported it, and demand management where specification rationalization could reduce spend without compromising quality or operations. The retail vendor consolidation was one workstream among several. Technology categories with high vendor margins and meaningful competitive alternatives were addressed through displacement-oriented negotiations. Core medical item spend was approached through a combination of demand management and enterprise pricing negotiations across the consolidated location base.

The $2.4 million in EBITDA impact, representing a 25 percent reduction across categories in scope, reflected the combined effect of these workstreams across everything from core medical supplies to SG&A. Retail was one element of a broader engagement. Beyond the direct savings, SKU rationalization in the retail segment reduced inventory by 20 percent and cut order-to-delivery time in half.

— Michael Ames, CFO, US Eye

That outcome was not the product of scale leverage. It came from category-level analytical rigor and disciplined application of the right savings lever to the right spend.

EBITDA impact for US Eye following rapid multi-practice acquisition, from procurement synergy capture across medical, technology, retail, and SG&A categories combined.

Spend reduction across categories in scope, with inventory down 20% and order-to-delivery time cut in half as operational byproducts of the same engagement.

What this means for healthcare CFOs and deal teams

The implications are practical and sequenced.

Before close, the synergy case for outside spend should be built from the bottom up, by category, not by applying a savings percentage to an aggregate number. Clean team protocols allow preliminary spend mapping against leverage opportunity without violating antitrust rules. The goal is not a precise number but a differentiated view: where is the leverage high, and which levers actually apply?

In the first 90 days post-close, focus on quick-turn demand management wins and the initiation of competitive evaluations in high-leverage categories. McKinsey’s framing of the Integration Management Office as “the deal’s operating system” applies directly here: procurement synergy initiatives that are not tracked to KPIs and assigned ownership will drift. The synergy case that was credible at signing will not realize itself.

Bain’s research on PE-backed healthcare M&A adds another dimension: revenue synergies are increasingly essential to justify valuations in the current environment, but they are also inherently riskier because they depend on market conditions and customer behavior. This dynamic raises the importance of cost synergy discipline, and specifically procurement, as the more controllable and predictable value driver.

For PE-sponsored healthcare platforms in particular, procurement synergy capture is not a one-time post-merger event. It is a repeatable capability that compounds across the hold period. Each acquisition adds spend, adds leverage, and adds opportunities for competitive displacement that did not exist before. Organizations that build this capability early create a structural cost advantage their competitors cannot easily replicate.

The bottom line

Healthcare M&A synergy capture is not fundamentally a technology problem, a culture problem, or a regulatory problem. It is an analysis problem and an attention problem. Most organizations apply meaningful rigor to organizational integration and labor cost management, then apply insufficient rigor to procurement, accepting a self-fulfilling outcome where low targets produce low effort, which produces low realization.

The available value is real. The analytical work to surface it is achievable. The firms that do it consistently outperform the ones that do not.

We run a no-cost spend assessment and give you a category-level view of where procurement savings are most likely, before any engagement begins.

Schedule a No-Cost Spend Assessment

Related Resources

Service Page

Healthcare Procurement Optimization & Transformation

Our full approach to outside spend reduction for multi-site operators and PE-backed healthcare companies.

White Paper

Capturing Procurement Value in Multi-Site Healthcare Acquisitions

A full operator playbook for PE sponsors and C-suite executives at multi-site healthcare platforms.

Case Study

US Eye: $2.4M EBITDA from Post-Merger Procurement Integration

How a PE-backed ophthalmology platform captured 25% spend reduction across categories in scope following rapid multi-practice acquisition.

Insight

Sourcing: The Most Underexploited M&A Synergy Lever

Why the easy synergies get priced in at signing, and how a category-level approach unlocks the value that remains.

Selected sources: McKinsey & Company, Capturing M&A Value: Cost, Capital, and Revenue Synergies (2026); McKinsey & Company, How Healthcare Entities Can Use M&A to Build and Scale New Businesses (2025); Bain & Company, Healthcare M&A Report (2022); Bain & Company, Bringing Science to the Art of Revenue Synergies (2022); Harvard Business Review, The New M&A Playbook (2011); IMAA Institute, Capturing Synergies in Health System M&A; NBER, Mergers and Marginal Costs: New Evidence on Hospital Buyer Power; Healthcare Finance News, summary of merger savings research; Inside Consulting client engagement data.