Industrials · Procurement Optimization & Transformation

Industrial Companies Are Leaving Significant Margin on the Table in Their Outside Spend

Inside Consulting delivers procurement transformation across direct materials, indirect spend, MRO, logistics, contract labor, and SG&A for mid-market and PE-backed aerospace, defense, and manufacturing companies. Average savings: 24%. Results-based fees.

Schedule a No-Cost Spend AssessmentThe Problem

Industrials Procurement Is Built for Continuity, Not Cost Performance

Mid-market manufacturers, defense contractors, and aerospace suppliers operate with procurement functions designed to keep the line running. Supplier relationships stretch back decades. MRO contracts auto-renew. Contract labor rates track the market without leverage. Freight gets booked at list. For PE-backed companies managing EBITDA targets, the unrealized savings in procurement represent one of the largest untapped value creation levers available.

Direct Materials Pricing Gaps

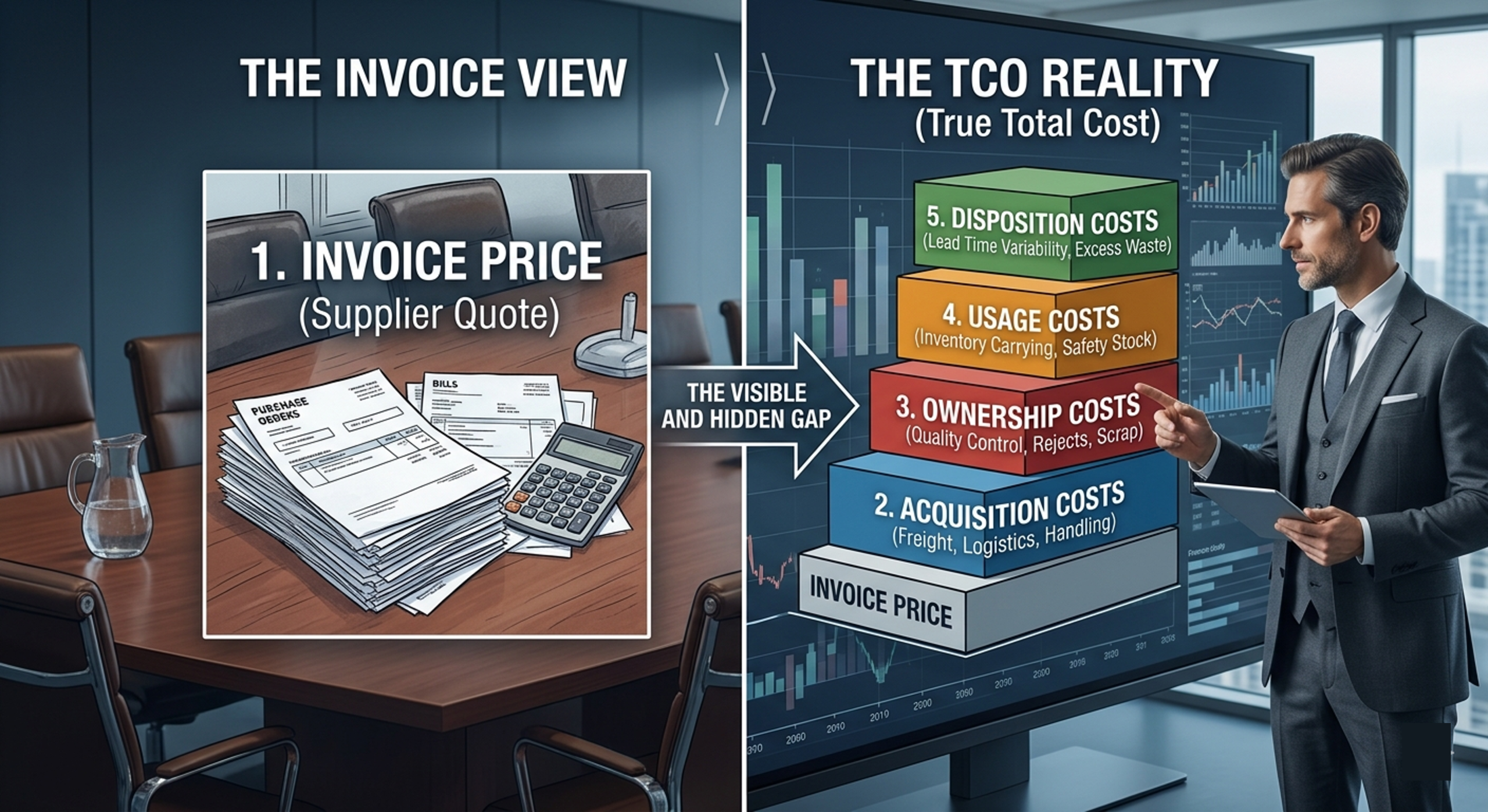

Raw materials, components, and specialized assemblies are often sourced from incumbent suppliers on legacy pricing that hasn't been tested competitively in years. Total cost of ownership analysis frequently reveals significant opportunities that per-unit price negotiations miss entirely.

MRO and Indirect Spend Neglect

Consumables, tooling, safety, and maintenance materials grow with operations but rarely attract procurement discipline. Supplier counts proliferate, catalog controls erode, and volume leverage goes unrealized across what is often 15 to 20 percent of total outside spend.

Contract Labor at Above-Market Rates

Staffing markups for skilled trades and engineering contingent labor run 15 to 25 percent above market at many industrial companies. Incumbent staffing relationships persist without competitive pressure because no one has bandwidth to run a sourcing event across every category simultaneously.

Tariff Exposure Without a Response Plan

Section 301 tariffs, Section 232 steel and aluminum duties, and evolving trade policy have created material cost increases for manufacturers sourcing globally. Most companies have absorbed the cost rather than developing a structured mitigation strategy across their supply base.

Fragmented Multi-Site Spend

PE-backed roll-ups often have five, ten, or more acquired entities each buying independently from overlapping supplier sets. Volume leverage that could command significant pricing improvements sits uncaptured because no one has consolidated the spend picture across the platform.

SG&A and Back-Office Costs Growing Faster Than Revenue

Professional services, benefits, insurance, technology, and back-office functions often receive less procurement rigor than operational categories. In aggregate they represent meaningful savings opportunity, particularly in companies that have grown through acquisition and accumulated redundant vendors.

What We Source

Procurement Category Coverage Built for Industrials Companies

We work across 100+ spend categories specific to industrial operators. Below are the highest-impact procurement cost reduction areas for aerospace suppliers, defense contractors, and PE-backed manufacturing platforms.

Manufacturing & Production

Direct Materials

- Raw materials (metals, polymers, composites)

- Engineered components and subassemblies

- Highly specialized and sole-source items

- Total cost of ownership (TCO) analysis

- Make-vs-buy analysis and restructuring

- Tariff exposure analysis and mitigation

- Multi-source qualification programs

- Long-term agreement structuring

Operations & Facilities

MRO, Indirect & Logistics

- MRO consumables, tooling, and safety

- Maintenance and repair services

- Inbound freight and outbound parcel

- LTL, truckload, and intermodal

- Facilities services (janitorial, security, landscaping)

- Utilities and energy management

- Capital equipment and leases

- Waste and environmental services

Workforce & SG&A

Labor, Services & Back Office

- Contract and contingent labor (skilled trades, engineering)

- Subcontractors and outside services

- Professional and consulting services

- Benefits and HR administration

- Insurance and risk management

- Back-office technology and software

- Corporate travel and fleet

- Office and administrative spend

Tariff Impact & Mitigation

Trade Policy Has Changed the Cost Structure of Industrial Supply Chains. Most Companies Are Still Absorbing It.

Section 301 tariffs on Chinese imports, Section 232 steel and aluminum duties, and a shifting global trade environment have materially increased costs for manufacturers and aerospace suppliers sourcing globally. The companies that have responded strategically are capturing cost advantages their competitors haven't found yet.

What We Find

Most industrial companies absorbed tariff increases as a cost of doing business rather than treating them as a structured sourcing problem. The result: suppliers passing through tariff costs that were never verified, classifications that may not be optimized, and supply base configurations that made sense before the tariff environment changed.

Inside Consulting conducts detailed tariff exposure analysis across your direct and indirect supply base, identifying where you are paying tariff-inflated costs, where alternative sourcing configurations can reduce or eliminate the exposure, and where first-sale and duty drawback mechanisms may apply.

Our Tariff Analysis Covers

- Section 301 exposure mapping across the supply base (List 1 through List 4B)

- Section 232 steel and aluminum duty impact on direct materials

- HTS classification review for potential reclassification opportunities

- Landed cost modeling: tariff-inclusive vs. alternative sourcing scenarios

- First-sale valuation and duty drawback applicability

- Near-shoring and friend-shoring analysis for tariff-sensitive categories

- Multi-source qualification to reduce single-country exposure

- Supplier negotiation to share or absorb tariff costs contractually

- Tariff exclusion and exemption monitoring and filing support

Our Approach

How Our Industrials Procurement Transformation Process Works

Inside Consulting runs industrials procurement transformation engagements end-to-end, from spend discovery through supplier negotiation to realized savings on the P&L. We bring the category expertise, analytical rigor, and sourcing process that most mid-market industrials companies don't have internally.

Spend Discovery

We map your full outside spend base across all categories, entities, and facilities. For industrials companies, this spans direct materials, MRO, contract labor, logistics, subcontractors, SG&A, and back-office costs. We identify the categories with the highest cost reduction potential and size the opportunity before any sourcing work begins.

Weeks 1–4What we do in this phase

- Extract and normalize accounts payable data across all entities and facilities

- Map spend by vendor, category, and site into a unified spend cube

- Identify supplier fragmentation and consolidation opportunities

- Flag tariff-exposed categories and assess Section 301/232 impact

- Assess contract status, auto-renewal exposure, and term gaps

- Deliver a prioritized opportunity map with savings estimates by category

Category Analysis

We analyze contracts, assess supplier leverage, and prioritize categories by savings magnitude and speed to capture. For direct materials, we conduct total cost of ownership analysis to size the full addressable opportunity beyond per-unit pricing. For tariff-affected categories, we model landed cost scenarios across alternative sourcing configurations.

Weeks 3–8What we do in this phase

- Assess contract terms, pricing history, and expiration dates by vendor

- Conduct total cost of ownership analysis for direct materials categories

- Identify make-vs-buy opportunities and restructuring options

- Model tariff-inclusive landed costs vs. alternative sourcing scenarios

- Size savings potential for each prioritized category

- Develop negotiation strategy and identify competitive sourcing options

Supplier Negotiation

We lead all supplier conversations, armed with cost analysis, competitive alternatives, and TCO data. We drive cost reductions without disrupting your operations, production schedules, or existing supplier relationships. For compliance-sensitive categories, all recommendations are structured around your operational and regulatory constraints.

Months 2–6What we do in this phase

- Run competitive sourcing processes (RFPs, reverse auctions, multi-round tenders) across targeted categories

- Lead all supplier conversations and commercial negotiations

- Apply volume consolidation leverage across multi-site and portfolio-wide spend

- Negotiate pricing, terms, service levels, and renewal structures

- Manage engineering and operations stakeholder alignment where relevant

- Qualify alternative sources for tariff-affected and single-source categories

Savings Realization

We track and verify savings against a defined baseline, ensuring negotiated commitments become captured EBITDA rather than projected opportunities that never materialize on the P&L. Our savings methodology is designed to hold up in PE due diligence and board reporting.

Months 3–9What we do in this phase

- Establish a verified savings baseline before any changes go live

- Track realized savings against baseline by category and supplier

- Confirm new pricing is honored in actual invoices and purchase orders

- Address off-contract purchasing and unmanaged supplier adoption

- Deliver regular savings reporting to finance and PE sponsors

Governance & Holdback

We document contracts, set renewal alerts, and install lightweight procurement governance so savings don't erode as your company continues to grow, hire, and acquire. We leave your team with the playbooks and category frameworks to sustain the savings without ongoing consulting fees.

Month 6 onwardWhat we do in this phase

- Build preferred supplier lists and purchasing guidelines by category

- Centralize contract storage and set expiry and renewal alerts

- Establish approval framework for new supplier onboarding

- Define integration path for future acquisitions into the supply base

- Hand off category playbooks, scorecards, and governance documentation

Client Results

Industrials Procurement Engagements, Delivered

A sample of our procurement cost reduction work in industrials, spanning manufacturing, construction materials, and global supply chain transformation.

Manufacturing · Direct Materials & Outside Spend

Swisslog

15%+ direct & indirect savings Plus $1M+ in labor savings from product and process redesign, and pricing improvements on spare parts

Healthcare automation manufacturer. Rapid profit improvement program spanning direct and indirect materials, make-buy restructuring on installations, and a product redesign that eliminated over $1M in annual labor cost.

View Case Study →Construction Materials · Supply Chain & Operations

Brassmonier

15–25% across categories Savings across purchasing via reverse auctions, multi-round tenders, energy strategy, and creative freight sourcing despite Jones Act constraints

$500M construction materials manufacturer. Rapid turnaround following an 80% drop in demand. Procurement transformation across purchasing, logistics, energy, and equipment strategy across a multi-plant network.

View Case Study →Selected industrials clients

Thought Leadership

Our partners write from experience, not theory. The pieces below represent the frameworks and findings we apply in industrials procurement engagements every day.

Why Inside Consulting

Built for Industrials Companies That Need Procurement Transformation Without Building a Department

Industrial companies on PE timelines can't wait for a 12-month assessment process. We move fast, go deep, and work on your timeline. Our team includes McKinsey- and BCG-trained partners with engineering backgrounds and careers serving Fortune 100 industrial and aerospace companies.

Industrials Domain Expertise

Our partners hold engineering degrees and have spent careers serving aerospace, defense, and manufacturing companies at McKinsey, BCG, and in operational roles. We understand how industrials companies buy, what drives total cost, and where the structural savings opportunities are.

TCO and Direct Materials Depth

We don't stop at per-unit price. Total cost of ownership analysis across direct materials, including raw materials, engineered components, and highly specialized items, routinely surfaces savings that traditional price negotiations miss. That depth is what makes the difference in complex manufacturing categories.

Tariff Strategy and Trade Policy Fluency

We have done deep analysis on tariff impact and mitigation across Section 301, Section 232, and evolving trade policy. That capability is increasingly central to direct materials cost reduction for manufacturers with any global sourcing exposure.

Results-Based Fee Structures

We offer engagement structures that tie our compensation directly to realized savings. Our fees are linked to what we actually deliver against a defined baseline. If we don't find savings, you don't pay the same. Period.

PE Fluent

We speak the language of private equity: EBITDA improvement, MOIC, value creation plans, and 100-day priorities. Our procurement engagements are designed to appear on a board deck and survive due diligence.

No Software. No Platform.

We don't sell a procurement platform or spend analytics tool alongside our services. Our only product is savings. That means no conflicted recommendations and no technology implementation dragging out the timeline.

What industrials procurement transformation actually looks like

Industrials procurement transformation is not a technology implementation, a spend analytics dashboard, or a consultant report with recommendations your team has to execute. It is the process of replacing fragmented, site-level supplier relationships with a structured, leverage-based supply strategy built on cost analysis, competitive sourcing, and governance that holds. Inside Consulting has executed this work for manufacturers, aerospace suppliers, and defense contractors at every stage of the PE hold cycle, from 100-day value capture through pre-exit margin improvement. The result is not just lower costs in one category. It is a supply base your organization can actually manage as it continues to grow, hire, and acquire.

Common Questions

Frequently Asked Questions

What is industrials procurement optimization consulting?

Industrials procurement optimization consulting is the systematic process of reducing what a manufacturer, aerospace supplier, or defense contractor spends with outside vendors across categories including direct materials, MRO, contract labor, logistics, subcontractors, and SG&A. A procurement optimization consultant analyzes current supplier contracts, identifies where the company is overpaying relative to what a rigorous competitive sourcing process would deliver, and leads negotiations to capture verifiable cost reductions. Inside Consulting does this work end-to-end for mid-market and PE-backed industrials companies, from spend mapping through contract execution and savings verification.

What does total cost of ownership analysis mean for direct materials?

Total cost of ownership (TCO) analysis goes beyond unit price to capture the full cost of acquiring and using a material or component. For industrials companies, this typically includes incoming quality costs, supplier-related production disruptions, expedite and premium freight costs, inventory carrying costs tied to supplier lead times, and any qualification or engineering costs associated with supplier changes. TCO analysis frequently surfaces savings opportunities that unit-price negotiations miss, particularly in engineered components and specialized materials where incumbent suppliers have historically faced little competitive pressure.

How do you approach tariff impact analysis and mitigation for manufacturers?

We begin with a detailed mapping of tariff exposure across the supply base, identifying which categories and suppliers carry Section 301 or Section 232 exposure and quantifying the landed cost impact. From there, we evaluate mitigation options: alternative sourcing configurations, near-shoring or friend-shoring opportunities where the economics support it, HTS classification review, first-sale valuation where applicable, duty drawback opportunities, and supplier negotiation to contractually share or absorb tariff costs. The analysis is grounded in actual landed cost modeling, not theoretical alternatives. Many manufacturers have absorbed tariff costs as a fixed input when a structured response would reduce or eliminate a significant portion of the exposure.

Will supplier changes disrupt our production or program delivery schedules?

We treat production continuity as a hard constraint, not a preference. For categories where supplier switching carries qualification risk, engineering approval requirements, or program delivery implications, our strategy focuses on renegotiating with existing suppliers rather than replacing them. We do not recommend changes that would create operational disruption unless the client explicitly asks us to evaluate that path. The categories where we apply the most competitive pressure are those with sufficient supply base depth to run a credible sourcing event without operational risk.

How do you handle multi-site or portfolio company engagements?

This is one of the highest-value applications of our procurement work. PE-backed industrials roll-ups often have five, ten, or more acquired entities each buying independently from overlapping supplier sets. We consolidate spend data across all entities, identify the categories where aggregated volume creates meaningful leverage, and negotiate on a combined basis. Individual site operational autonomy is preserved where it matters; aggregated purchasing leverage is applied where it doesn't. We also structure the supplier onboarding process for future acquisitions so each new entity enters a managed supply base rather than perpetuating fragmentation.

What does a results-based fee structure look like?

Under a results-based structure, a portion of our fees is linked to verified, realized savings rather than time spent or projected estimates. We work with you to define a savings baseline and measurement methodology at engagement start. Our compensation is then tied to what we actually deliver against that baseline. We also offer hybrid models that combine a retainer component with a results-based component, which works well for companies that need billing predictability while still aligning our incentives with outcomes.

We already have a procurement team. Why would we need outside help?

Most mid-market industrials companies have procurement staff focused on direct materials continuity and supplier relationships tied to active production. Indirect spend, MRO, contract labor, logistics, and SG&A categories rarely get dedicated bandwidth or rigorous competitive sourcing. We run in parallel with your team, take on the categories they don't have capacity for, and bring the category depth and sourcing process rigor that most internal teams aren't resourced to apply across 15 to 30 categories simultaneously. The result is savings that wouldn't otherwise be captured without meaningfully burdening your existing team.

How long does a typical engagement take?

Engagements typically run six to twelve months. The spend discovery and baseline phase takes three to four weeks. First negotiated savings are typically documented within ninety days of engagement start. The full program runs through category analysis, competitive sourcing events, contract execution, and supplier transition, with governance and capability-building at close.

Find Out What Your Industrials Company Is Overpaying in Outside Spend

We'll run a no-cost spend assessment and give you a category-level view of where procurement savings are most likely, before any engagement begins.

Request a Spend Assessment See Our Full ApproachMore from Inside Consulting

How Inside Consulting drives procurement savings for health systems, physician groups, and PE-backed healthcare platforms.

Service Page Technology Procurement Optimization & TransformationSaaS, cloud, and corporate spend reduction for growth-stage and PE-backed technology companies.

Article Procurement as a Value Creation Lever in PE-Backed IndustrialsHow operating partners use procurement transformation to expand EBITDA in manufacturing and aerospace and defense platforms.

Get Started Talk to an Inside Consulting ExpertTell us about your spend profile and we'll show you where the opportunity is, before you commit to an engagement.