The Growth Tax: Why Growth-Stage Companies Overpay for Their Tech Stack, and How CFOs Can Close the Gap

As growth-stage companies scale from Series A through Series C, vendor contracts priced for an earlier, smaller business quietly drain margin. The gap between what you pay and what your purchasing power should command is the Growth Tax.

Inside Consulting | CFO Perspective

Dan Bleicher, Partner, Inside Consulting

Published April 2, 2026

Executive Summary

Growth-stage companies are uniquely vulnerable to a hidden cost problem: vendor contracts priced for a smaller, earlier version of the business. As revenue scales from Series A through Series C, purchasing volume rises substantially, but pricing rarely follows.

The result is the Growth Tax: a widening gap between what a company pays and what its current purchasing power should command. For a Series B or C company, this gap typically represents 15% to 30% in recoverable savings across outside spend categories.

This paper explains how the Growth Tax forms, which spending categories carry the most risk, and what a systematic approach to closing the gap looks like in practice.

1. A Problem Hidden in Plain Sight

Every fast-growing company knows what it costs to acquire customers, retain employees, and build product. But ask a Series B or Series C CFO what their per-seat CCaaS cost was when their contract was signed versus what comparable volume commands in today’s market, and the answer is often silence.

That silence has a dollar value.

Rise in SaaS cost per employee over just 24 months

Vertice, 2026

Share of vendors that deliberately obscure price increases at renewal

Vertice, 2026

Extra cost from unoptimized vendor relationships

Ardent Partners

SaaS costs per employee reached approximately $9,100 by end of 2025, up from $7,900 just two years prior (Vertice, 2026). Research from NPI Financial found that companies overspend on approximately 85% of their IT purchases. The root cause is not negligence. It is the nature of how vendor relationships are established during early growth stages and rarely revisited at scale.

2. How the Growth Tax Forms

The Growth Tax is not a single event. It is the cumulative result of three dynamics that compound quietly over the arc of a company’s growth.

Pricing Locked at Series A

Vendors price to the customer’s size at signing. As revenue scales from $3M ARR to $25M+, that early pricing rarely resets automatically.

Auto-Renewals by Inaction

Annual contracts with 30–90 day notice windows renew silently. Finance teams focused on growth rarely flag these windows in time.

Category Sprawl

Functions procure in silos independently. Aggregate volume in any category is invisible to vendors and to internal teams alike.

By Series B, the median ARR for a B2B SaaS company reaches approximately $10 million (SaaStr, 2024). By Series C, revenue is often in the $25M to $75M range. The company buying CCaaS seats at Series C is a fundamentally different buyer than it was at Series A. The contract often is not.

3. Where the Growth Tax Hits Hardest

Three categories consistently represent the highest concentration of recoverable value for growth-stage technology and financial services companies.

Typical recoverable savings on renegotiated outside spend at Series B/C companies

15–30%

Concentrated in CCaaS, customer engagement platforms, and back-office SaaS

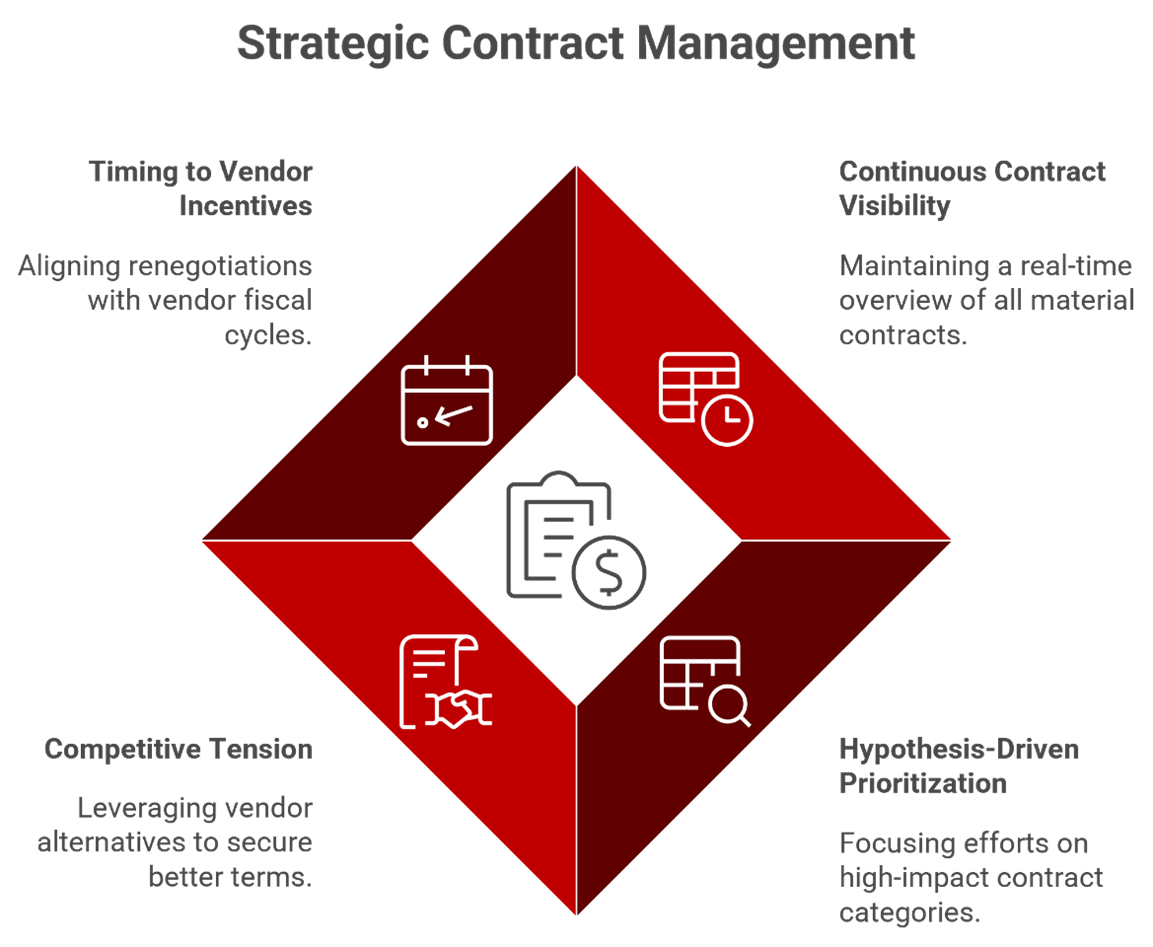

4. What Best-in-Class Looks Like

Companies that close the Growth Tax gap share a common set of practices. None require ripping out incumbent vendors. They require discipline, structure, and the willingness to treat outside spend as an active financial lever rather than a fixed cost line.

Timing to Vendor Incentives

Vendor fiscal year-ends and quarter-ends create natural pressure points. Aligning renegotiation conversations to vendor calendars captures concessions that evaporate with poor timing.

Continuous Contract Visibility

A rolling view of every material contract (expiration dates, renewal windows, current pricing, utilization, and the delta vs. market rate) embedded in the financial planning cycle.

Competitive Tension

Vendors respond to credible alternatives. Building a realistic assessment of competitive options and communicating it transparently consistently delivers better outcomes than loyalty-based negotiation.

Hypothesis-Driven Prioritization

Concentrate effort on categories where high spend, recent growth, and high market competition create the greatest leverage. Not every contract warrants equal investment.

In commoditized categories like CCaaS, telephony, and email infrastructure, a structured competitive process can deliver reductions of 20% or more without switching vendors, simply by creating a credible alternative to the status quo. Vendor fiscal year-ends and quarter-ends create natural pressure points where this approach is most effective.

5. The CFO Self-Diagnostic

The five questions below are a starting point for assessing where your Growth Tax exposure is greatest. Check YES or NO. Two or more NO answers signals meaningful recoverable value.

| # | Diagnostic Question | YES | NO |

|---|---|---|---|

| 1 | Have your vendor contracts been renegotiated since your last funding round? | ☐ | ☐ |

| 2 | Do you have visibility into actual usage vs. contracted seats or volumes across your SaaS stack? | ☐ | ☐ |

| 3 | Are your CCaaS or telephony contracts priced based on your current headcount and volume? | ☐ | ☐ |

| 4 | Do you have a systematic process for managing renewal dates and triggering renegotiation windows? | ☐ | ☐ |

| 5 | Have you benchmarked your current vendor pricing against market rates in the past 12 months? | ☐ | ☐ |

2–3 NO answers: Meaningful gap exists.

4–5 NO answers: Significant Growth Tax likely in progress.

6. The Bottom Line

Outside spend is one of the most undermanaged levers available to a growth-stage CFO. The revenue function gets attention. The headcount function gets attention. Vendor contracts tend to be renewed by inaction and optimized only during moments of crisis.

For a company at Series B or Series C, the window between rounds is precisely the moment when this work pays off most. Revenue is growing. Volume is up. Market alternatives are plentiful. The ingredients for a strong renegotiation are in place. What is often missing is a structured approach to capturing the value.

The Growth Tax is not inevitable. It is a gap between what growth-stage companies pay and what their current purchasing power should command. Closing that gap is not a procurement exercise. It is a margin improvement initiative that belongs on the CFO’s agenda.

Ready to quantify your Growth Tax exposure?

Inside Consulting works with CFOs and PE sponsors to identify recoverable savings, execute vendor renegotiations, and build the contract visibility infrastructure that prevents the Growth Tax from returning.

[email protected] | insideconsulting.net

About the Author

Dan Bleicher Partner, Inside Consulting

Dan is a Partner at Inside Consulting with more than 11 years of management consulting experience, including McKinsey & Company. He specializes in procurement transformation, supply chain optimization, and operational value creation across healthcare, pharmaceuticals, and advanced industries. Dan graduated from the United States Naval Academy and earned an MBA from Dartmouth’s Tuck School of Business.

Sources

Vertice. SaaS Inflation Index 2026 Report. vertice.one.

Ardent Partners. Procurement Research. As cited in PRGX, “Why Contract Renegotiation is the Perfect Time to Optimize Supplier Relationships,” 2025.

NPI Financial. “IT Vendor Management Best Practices to Cut Costs.” npifinancial.com.

Gartner. As cited in various SaaS industry reports, 2023–2024.

SaaStr / 20VC / La Famiglia. B2B SaaS Benchmarks. As reported in VC Cafe, 2024.

Getmonetizely. “Procurement Guide: How Contact Center as a Service (CCaaS) Solutions Are Priced for Enterprises,” 2025.

Forrester Research. CCaaS Market Overview, 2023.